Accounting 101

We have to understand the mechanisms of the things that we work with every day. The small business owner has to have a grip on accounting, mark-ups & margins, stock and overheads.

For our course on basic accounting: please see:

https://moneyflows.co.za

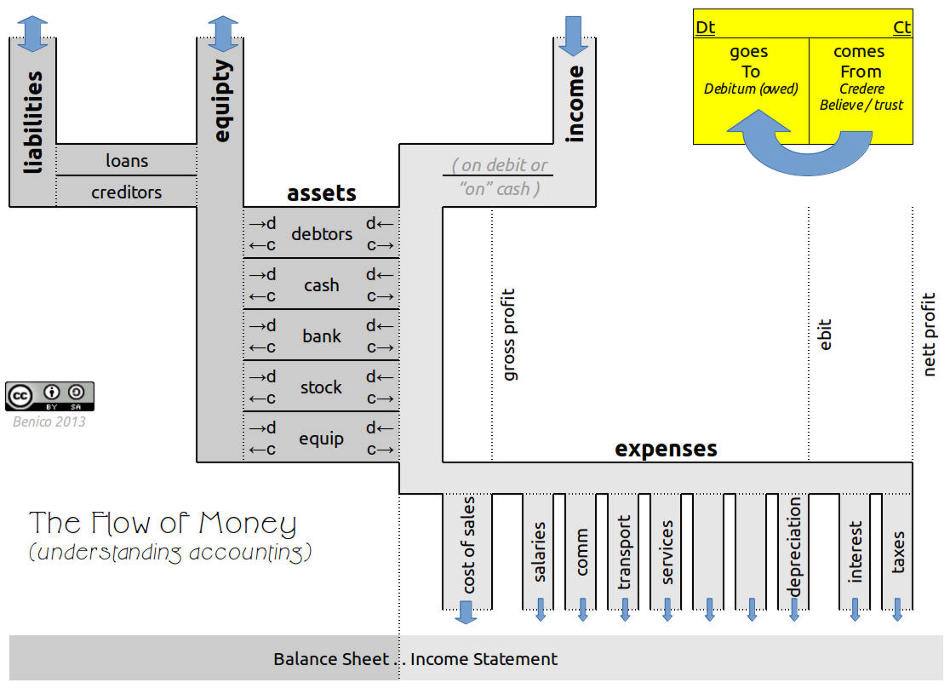

Accounting is about the FLOW of MONEY

Key concept 1:

"came from" and "went to"

You have to account for:

- where did the money COME FROM (credit this account) (entry on the credit side (right side) of the T account) and

- where did the money GO TO(debit this account) (entry on the debit side (left side) of the T account)

Key concept 2:

"All Inflow is NOT Income, All Outflow is NOT Expense"

If money flows into a business and you must give it back it is NOT income.

If money flows out of a business and you can get it back or you are giving it back, it is NOT an expense !

INCOME - EXPENSE = PROFIT and profit belongs to the OWNERS

Key concept 3:

"3 ways in & 3 ways out"

There are only three ways (modes / means of) money can flow INTO a business:

- From the owners (Equity) , (have to give this back)

- From borrowing (Liabilities), (have to give this back)

- From Income, (don't "owe" this to someone, don't have to "give it back")

There are only three ways (modes / means of) money can flow OUT OF a business:

- To the owners (Equity) , (giving it back)

- To repaying loans (Liabilities),(giving it back)

- To Expenses, (can't "get this back")

Why is Equity + Liabilities = Assets

because all the Assets that are IN the business was either financed by the Owners or via Loans.

Examples:

- When the owner put money into the business ... it flows from equity (credit owner) to asset (debit bank).

- When you take money from the bank and buy stock ... it flows from one asset (credit bank) to another asset (debit stock).

- When you sell goods ... money flows from income (credit sales) to asset (debit bank) ... AND your client takes the goods from your stock (credit stock) and walks out of the door (debit cost of goods sold.)

- When you buy fuel ... money flows from the asset (credit bank) to the expense (debit fuel).